You’ve probably seen people with bold financial plans: “I’ll save £50,000 in five years” or “I’ll retire at 50” or “I’ll invest vigorously after paying off debt.” These visions are powerful, motivating, exciting, aspirational. But more often than not, they stay plans. Why? Because without small consistent actions, big ambitions tend to stall.

Tiny daily habits are like the bricks under the giant structure of your financial future. Each small, repeated action, checking your budget, automating a transfer, avoiding one impulse buy, might feel trivial, but over weeks, months, and years, those bricks add up. In fact, they often matter more than the grand plans, because a plan without execution is just a dream.

This article shows why tiny routines matter more than big blueprints, how to build them, and how they can quietly, steadily amplify your financial progress.

Habit vs Plan: Why Even the Best Plan Fails Without Action

A big financial plan has its place; it sets direction, gives purpose, and helps you visualise your future. But without repeated, daily follow-through, even the best plan stays in your head or notebook. Why so many plans fail:

- Overwhelm & inertia: Big goals feel massive. They can paralyse you because you’re unsure where to start or feel it will take forever.

- Motivation fades: At first, you’re fired up. But life intrudes, unexpected costs, busy workdays, fatigue. Without habits, what once felt urgent or exciting becomes optional or postponed.

- Lack of consistency: Big plans often depend on big action, which demands strength, time, or money. Daily habits, by contrast, require little but repeated consistency.

Tiny habits bridge the gap. They make progress inevitable, because they anchor effort to things you already do, and build momentum even when things are messy.

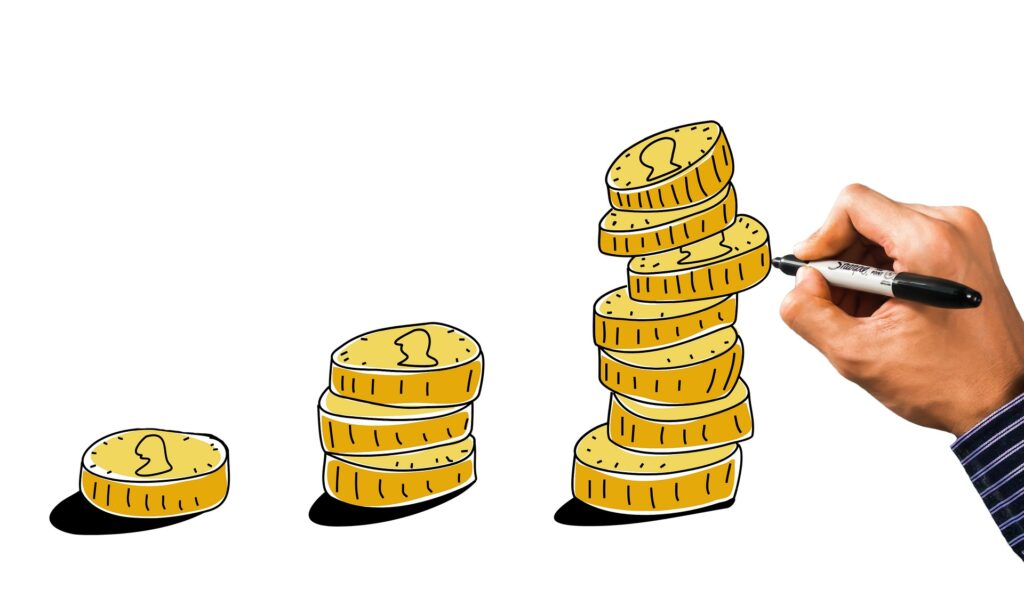

The Compound Effect of Small Actions

One small action repeated over time compounds, not just in savings or debt-reduction, but in mindset, confidence, and behaviour. Think of compounding not only in finances but in behaviour: tiny wins build trust with yourself, make you believe you can manage money, which in turn encourages more good actions.

For example, putting aside just £2 daily into savings seems negligible. But over a year, that’s nearly £750. Over five years, with modest interest, it grows significantly. Similarly, checking your bank app each morning for a minute may seem trivial, but it increases awareness, reduces wasted spending, and helps catch charges or fees early.

These small routines are powerful because they require low effort yet produce steady growth. When your habits are aligned and consistent, they become self-sustaining.

How to Build Tiny Habits That Stick

To make small habits real, you need a structured way to build them. Here’s how:

- Start super small: If you want to save more, start by saving just £1 or £5 a day. If you want to invest, maybe focus first on reading about investments daily. The key is that the action is so easy you’ll do it even when you feel tired.

- Anchor to something existing: Habit stacking helps. Link the new tiny habit to something you already do. After you have your morning tea, transfer your daily savings; after you finish dinner, review a purchase you made that day.

- Use triggers/reminders: Put sticky notes, set phone alerts, use visual cues. These work as prompts until the habit is internalised.

- Celebrate small achievements: When you do the habit, no matter how small, acknowledge it. A small self-pat on the back reinforces behaviour neurologically, you feel a bit of success, reinforcing further action.

- Adjust gradually: Tiny habits should feel manageable. If missing the habit becomes frequent, reduce the frequency, simplify the task, or adjust your timing.

Examples of Powerful Tiny Habits for Financial Growth

Here are concrete tiny habits that can deliver big rewards:

- Transfer £2-£5 automatically to savings every day (or weekly if daily is too frequent).

- Check one bank or card statement each morning or evening to catch unexpected charges.

- Pause 24 hours before any non-essential purchase to reduce impulse buys.

- Every payday, set aside a fixed percentage (even 2-5%) for investments or pension contributions.

- Cancel or pause one subscription or service you no longer use each month.

- Each week, identify one small thing you overpaid for and switch to a cheaper alternative or negotiate.

Each of these seems small, but together they shift your financial trajectory.

Why Small Habits Have Psychological Power

Tiny habits succeed where big goals fail partly because they leverage human psychology:

- Reduced friction: The smaller the action, the less resistance. When doing something feels easy, you’re more likely to do it.

- Frequent wins: Small consistent actions give regular feedback. That feeling of doing something, however small, keeps you motivated.

- Lower cognitive load: Massive tasks require significant planning and willpower; tiny habits are almost autopilot, freeing mental space.

- Identity building: When you repeatedly do small actions, you begin to see yourself as someone who follows through, this amplifies consistency.

These psychological effects support financial consistency more sustainably than high-energy attempts at large plans that are hard to sustain.

How Tiny Habits Outperform Big Goals in Busy Seasons

Life has seasons, work becomes intense, family obligations spike, stress takes over. In those moments, big plans often feel like extra weight. That’s when tiny habits shine:

- When time is scarce, you can still do a tiny action (e.g., saving a token amount, reviewing spending).

- When energy is low, you can still do something small instead of giving up completely.

- Tiny habits act as anchors; you keep a connection to your financial goals, even if you’re not moving full speed.

In this way, consistency doesn’t drop to zero; it dips, yes, but doesn’t collapse. Big plans without backup habits are brittle; tiny habits make the structure resilient.

Turning Tiny Habits into Bigger Outcomes

Tiny habits aren’t ends by themselves, they are stepping stones to larger financial outcomes. Over time:

- The small habits build up savings that can become emergency funds.

- That awareness from reviewing spending leads to better decisions, cutting waste, redirecting funds.

- Automatic transfers feed into investments, pensions, or property funds.

- Small wins build confidence which makes it easier to accept larger, wise financial decisions.

Before you know it, what started tiny becomes substantial: debt reduced, net worth improved, financial options expanded.

Overcoming Common Barriers

Even small habits hit resistance. Some typical hurdles and how to address them:

| Barrier | Solution |

|---|---|

| Skipping habit when busy or tired | Simplify further, if £5 saving feels too much, start with £1, or do habits at a fixed time when you are more likely to do them (morning, before bed). |

| Losing motivation fast | Track progress visually; record small wins; remind yourself why the goal matters. |

| Forgetting | Use reminders, prompts, anchors; habit stacking helps. |

| Believing small won’t matter | Do the math or run small tests, see how much those pennies saved or invested grow over a year or more. |

| Perfectionism | Accept that consistency matters more than perfection. Missing a day isn’t failure, just keep going. |

Big financial plans are great for direction and purpose, but they aren’t enough on their own. It’s the tiny daily habits, easy, consistent routines, that shape real progress. These are the actions you’ll maintain during busy seasons, the behaviours that compound into wealth, confidence, and financial security.

Don’t wait for the perfect moment. Start small, pick one tiny habit today, anchor it, do it, celebrate it and let momentum build. In time, those tiny habits will not just support your big plans, they’ll become the foundation that makes them possible.